I'm sorry for the absence, but the work has kept me pretty busy lately (and that's a good thing!).

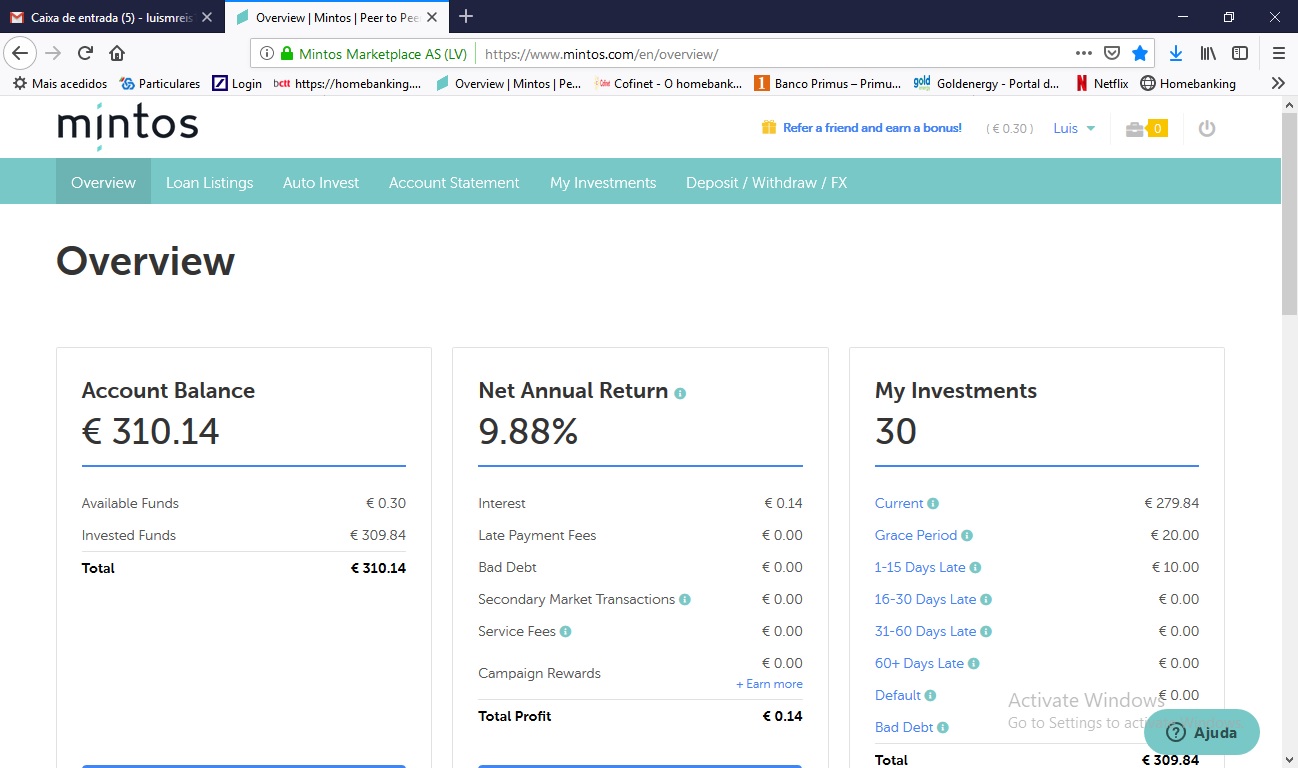

In the meantime, I "cashed" my first euro! I told everyone at work, and now I want to tell you too! It's silly, it's only € 1, but it's my first on this platform and I'm happy about it.

During the last few weeks I have selected short-term loans for two reasons:

1) Annual interest rates are much higher than in long-term loans

2) Liquidity is higher both because the sale of the loan is easier to sell and because the maturity of the principal is very short

1) Annual interest rates are much higher than in long-term loans

2) Liquidity is higher both because the sale of the loan is easier to sell and because the maturity of the principal is very short

My diversification among LO's is not homogeneous. I want to keep the annual interest rate high and this limits me to a bit of diversification, however, I am satisfied with the percentages of each LO.

The great advantage of entering the platform gradually is that I have time to learn from my mistakes, to see what works best and what I should not do. I continue to follow the groups on Facebook and some blogs over this and other platforms and I believe that soon I will enter into two others.

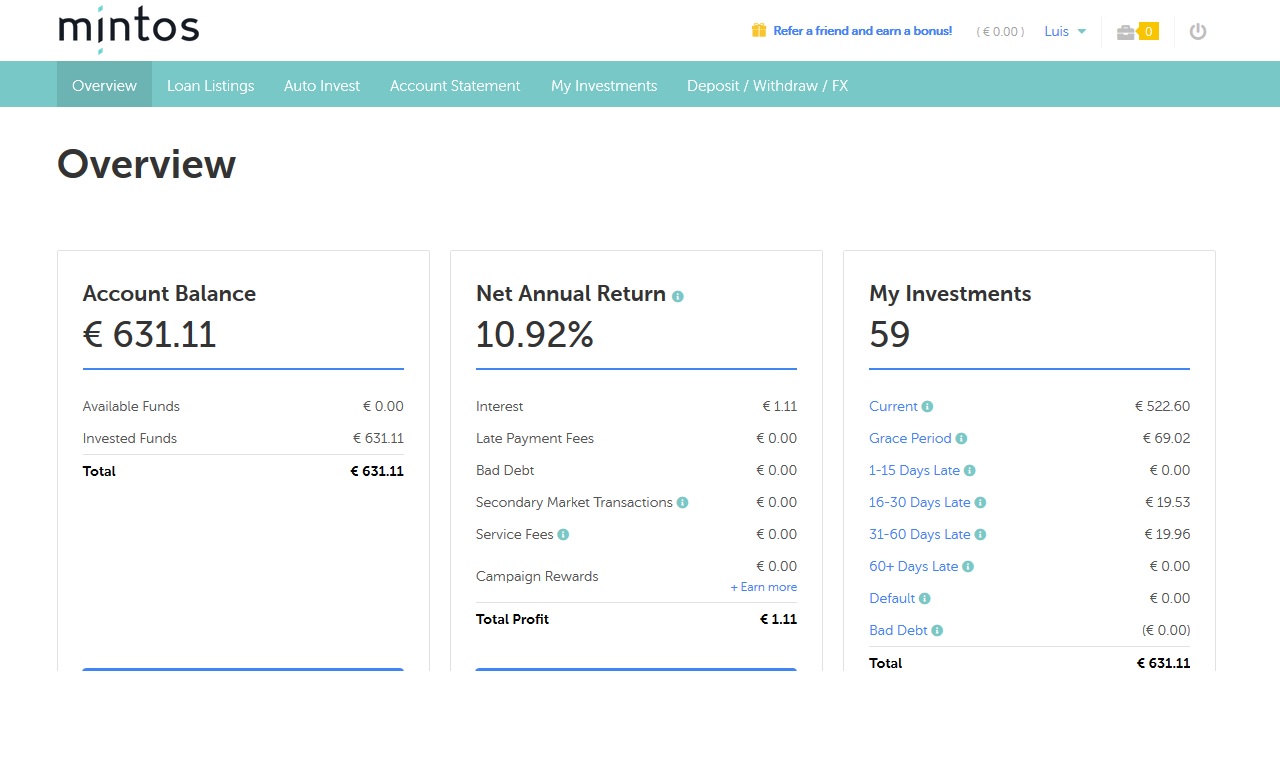

Seeing interest coming into our account almost every day is a motivating factor. However, seeing loans that are repaid before the term that had been established is unpleasant because the loans that are paid before their maturity are exactly the ones that have the best interest rates. Law of supply and demand, there is not much that can be done about it.

Regarding the cashback and agricultural loans announced by Mintos this week, I will not subscribe to either of these two hypotheses. Low interest, no buyback and long terms are not for me.

I wish you good investments!

I wish you good investments!